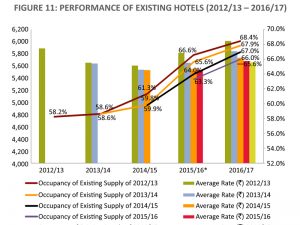

All major markets in terms of hotel performance have witnessed an increase in RevPAR except for Agra, according to HVS’ Trends & Opportunities survey. Noida (including Greater Noida) saw the highest year-on-year growth in RevPAR (16.0%), followed by Hyderabad (11.4%) and Ahmedabad (10.7%). Mumbai continues to lead in terms of both occupancy (74.2%) and average rate (`7,693) for the third year running. Noida displayed the lowest occupancy (56.9%) and Ahmedabad, the lowest average rate (Rs 3,840). All 13 hotel markets depicted an increase in occupancy leaving Pune (-0.7%), even as some markets saw a lower growth (Bengaluru and Mumbai at 0.4% and 0.6%, respectively) compared to others (Ahmedabad and Noida at 12.0% and 11.7%, respectively). In 2016-17, only two cities showed a decline in average rates – Agra, which witnessed a steep decline of 8.9% over 2015/16 and, Ahmedabad, which witnessed a minor decline of 1.1%. Goa registered the highest year-on-year increase of 7.3% in average rate, followed by Pune (5.7%).

Read More »

Tourism Breaking News

Tourism Breaking News